Retirement Income, Taxes, and Medicare in One Plan

The right platform connects Social Security, taxes, and Medicare IRMAA in one plan. Here is what to look for — and how RetirementAdvisorPro does it.

For a financial advisor, the best Social Security planning software is the platform that treats the filing decision as one piece of a complete retirement income plan — not a standalone calculation. RetirementAdvisorPro was built around that idea: it pairs claiming strategies and break-even analysis with the two costs most tools ignore, federal taxation of benefits and Medicare IRMAA surcharges.

That distinction matters more than any feature list. The 2026 T3/Inside Information survey found that more than half of advisors now use a dedicated Social Security analysis tool. The ones who stand out show clients not just the month that maximizes a lifetime benefit amount, but what that decision does to the tax bill and Medicare premiums that follow it.

Between ages 62 and 70 there is no single obvious month to file — there are thousands of possibilities. Research from the Social Security Administration shows that when filing ages are measured by month rather than year, a married couple faces more than 9,000 possible combinations, before survivor options are even considered. No one can test every Social Security filing age by hand.

Most households get it wrong. A landmark 2019 United Income study found that only 4% of retirees file at the financially optimal time, leaving an average of $111,000 per household on the table — roughly $3.4 trillion collectively. The math explains why: full retirement age is 67 for anyone born in 1960 or later, and filing at 62 permanently reduces the check by about 30%. Waiting past full retirement age earns delayed credits of 8% per year, reaching 124% of the primary insurance amount at 70. Social Security cost-of-living adjustments compound the gap — the 2026 COLA of 2.8% lifted the average retired-worker check to about $2,064 per month.

Guessing, or leaning on a rule of thumb, is the most expensive way to make a once-per-lifetime claiming decision — one that anchors a household’s income security for decades.

Free tools have a real place. The SSA’s free calculators produce quick benefit estimates from an actual earnings record, and free benefit calculators can frame the basic trade-off between filing early and waiting.

But those tools stop at the benefit itself. They cannot see a household’s IRA withdrawals, Roth conversion timing, spousal and survivor coordination, or the MAGI thresholds that drive Medicare surcharges. Benefit projections tell clients what they will receive; they say nothing about what they will keep. The gap between those two numbers is where an advisor earns the fee — and where real retirement security is won or lost.

Whether you evaluate RetirementAdvisorPro or any other Social Security platform, hold every tool to the same standard: it should model the whole household and the whole planning picture, not a benefit in isolation.

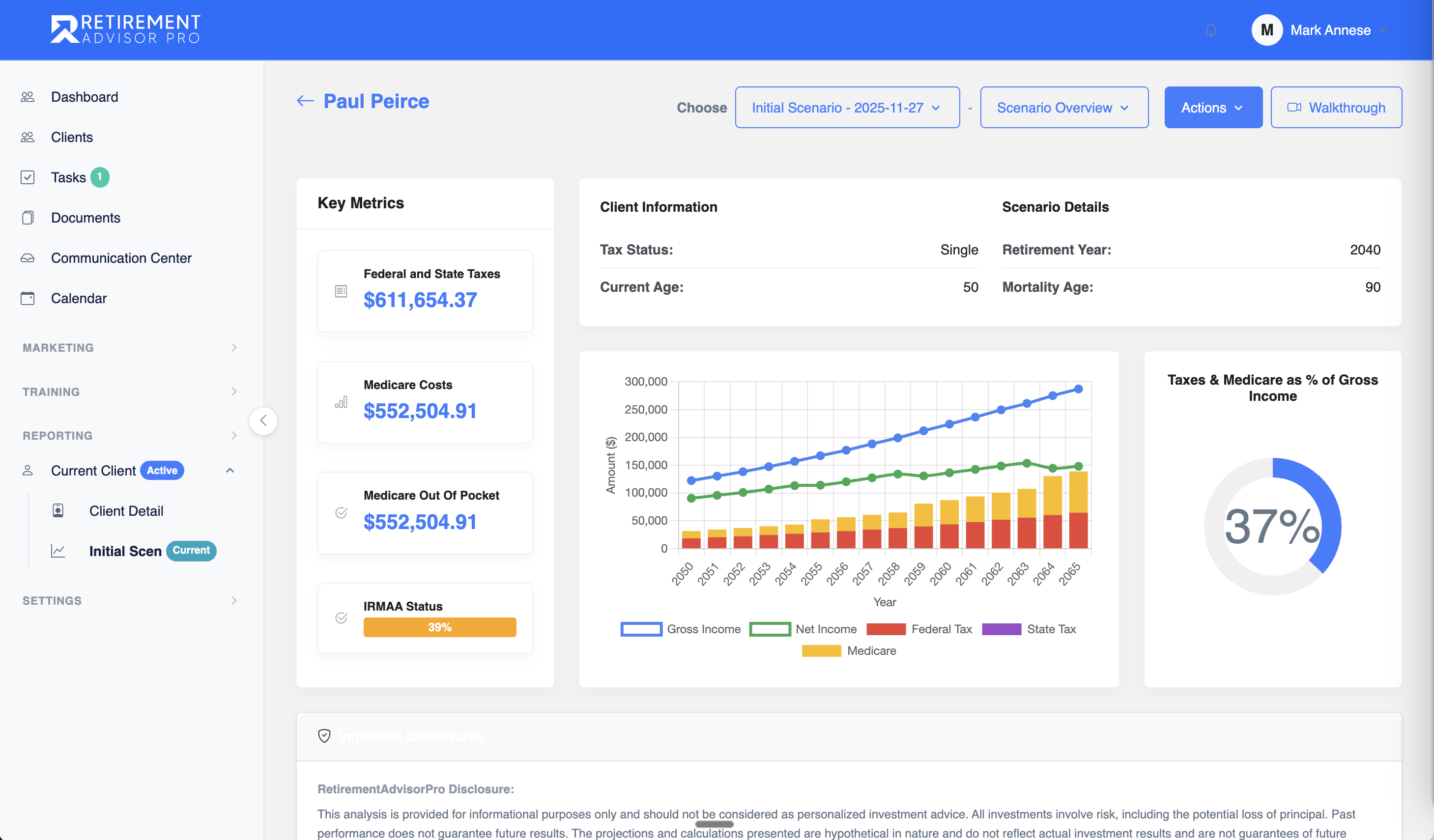

RetirementAdvisorPro treats Social Security maximization as an input, not the goal. The platform compares every filing age as a complete filing strategy, then layers on what happens after the check arrives: how much of it is taxable, whether it crosses an IRMAA bracket, and how the timing interacts with Roth conversions and required minimum distributions.

Advisors run Social Security filing scenarios beside a combined Medicare and Social Security stress test, model a Roth conversion and see its IRMAA consequences before recommending it, and generate unlimited client-ready reports. When clients ask how to maximize a benefit, the answer arrives with the taxes and premiums already attached.

Because the plan already contains the client’s MAGI and IRMAA exposure, the filing recommendation is never made in a vacuum. That is the difference between a standalone tool and a complete retirement plan.

The fastest way to judge any planning platform is to run a real case through it. Watch the Social Security demo, or book a live demo below and we’ll model one of your households — filing ages, taxes, IRMAA exposure, and Roth conversion timing — on the call.

Then keep exploring the rules behind every Social Security recommendation — the brackets, thresholds, Medicare costs, and tools that shape a client’s net retirement income and long-term security.

Benefits & Filing

IRMAA & MAGI

Brackets & Premiums

Common questions about our platform and services

Join financial advisors who are providing world-class retirement planning services with our AI-powered platform.