One Conversion, Three Systems: Brackets, the OBBBA Deduction, and IRMAA

A $100,000 Roth conversion can add $112,000 of taxable income and queue up an IRMAA surcharge two years later. Here is the full worked math for 2026.

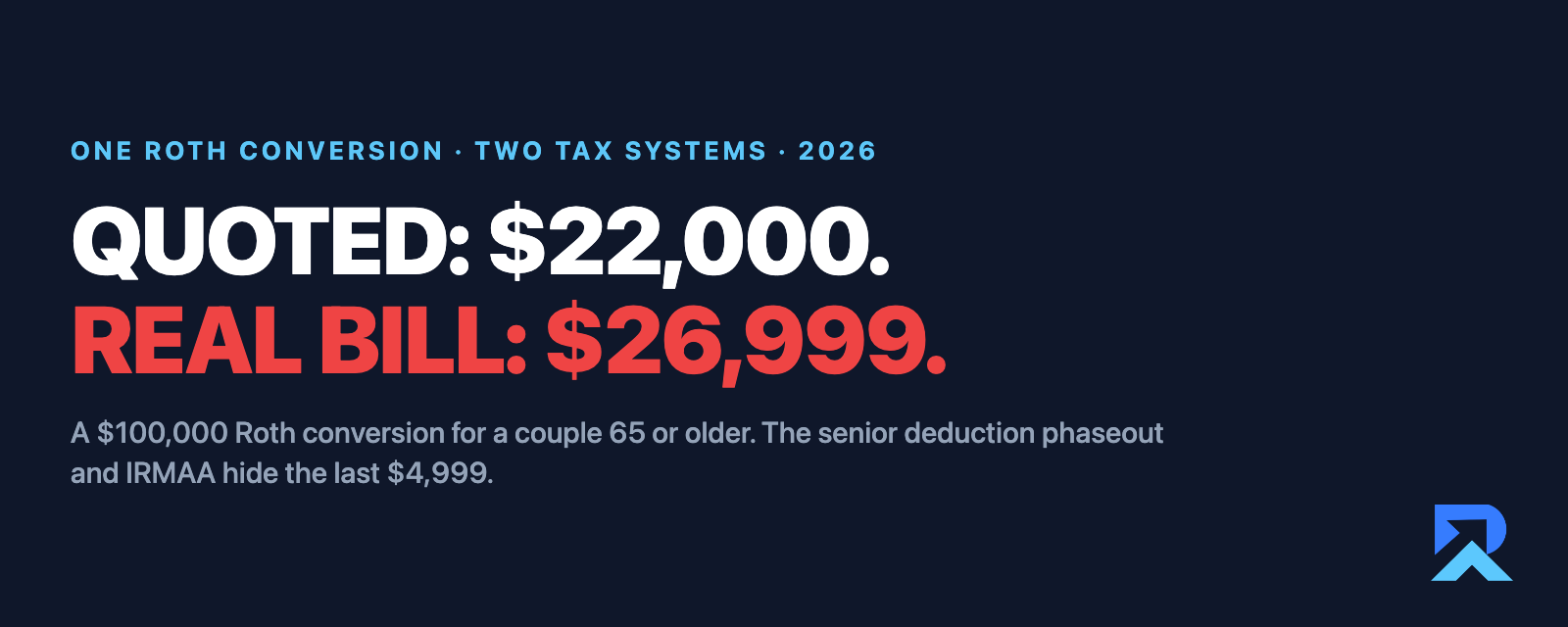

A Roth conversion can now cost meaningfully more than the tax bracket suggests, because the new senior deduction phases out as MAGI rises and IRMAA follows two years behind. In the worked example below, a married couple both 65+ converts $100,000 at $150,000 of MAGI — and the all-in cost is $26,998.80, a 27.0% effective rate, not the 22% the bracket table promised. We built the scenario using the IRS’s 2026 inflation adjustments (Rev. Proc. 2025-32) and the 2026 IRMAA thresholds, and verified every figure by hand.

The gap comes from two costs that never appear in bracket math: $2,702 of extra taxes from a fully erased $12,000 senior deduction, and $2,296.80 of IRMAA surcharges that arrive in 2028. Roughly $5,000 of hidden cost on one decision. Morningstar puts it plainly in “4 Smart Moves to Cut Your 2025 Tax Bill Under New Rules”: “If you are a senior who is close to the $150,000 MAGI limit, a large Roth conversion could easily push your income over the threshold, causing you to lose this entire $12,000 deduction.”

The One Big Beautiful Bill Act created a $6,000 senior deduction per person age 65 or older — $12,000 for a married couple when both spouses qualify — for tax years 2025 through 2028 only, according to IRS guidance on the 2025 tax law. It stacks on top of the regular standard deduction and the existing age-65 addition, and taxpayers claim it whether or not they itemize when they file.

Two design details drive everything in this article. First, the tax break phases out: each person’s $6,000 shrinks by 6% of MAGI above $75,000 for singles or $150,000 for married couples. For a couple where both spouses are 65 or older, both $6,000 amounts erode against the same joint excess — an effective 12 cents lost per dollar of MAGI over $150,000, with nothing left at $250,000.

Second, it is a below-the-line deduction. It reduces taxable income, but it does not reduce AGI or the MAGI that Medicare uses for IRMAA. That asymmetry is the trap: income that destroys the tax break gets no offset from it when the IRMAA calculation measures the same year’s MAGI.

A Roth conversion is the cleanest possible collision with these rules, because every converted dollar lands in ordinary income and MAGI in the conversion year. The bracket cost is visible. The phaseout cost and the IRMAA cost are not.

For most seniors, the appeal is simple: it is an additional deduction that lowers their taxable income without itemizing. Taxpayers 65 and older may claim it on top of the standard deduction — $32,200 for a married couple filing jointly in 2026, plus $1,650 for each spouse 65 or older, per IRS Rev. Proc. 2025-32 — so a qualifying couple can shield up to $47,500 of income from federal taxes before the phaseout begins. Seniors filing as singles get $6,000 with the phaseout starting at $75,000. In the 22% bracket, the full senior tax deduction is worth up to $2,640 of tax savings on a joint return.

Coverage from AARP and the Center for Retirement Research has framed the enhanced deduction as meaningful relief for middle-income seniors, and for many taxpayers it is. Two corrections matter for client conversations, though. First, the new tax deduction does not change how Social Security benefits are taxed — up to 85% of benefits remain taxable under the usual provisional-income rules, despite widespread claims that the 2025 law made Social Security tax-free. Second, higher-income seniors are phased out entirely, so the households most likely to be weighing large Roth conversions are exactly the ones whose taxes this article’s math applies to. Advisors who file this away now will spend less of the 2027 filing season correcting expectations on clients’ returns.

Take a married couple filing jointly, both spouses 65 or older, with $150,000 of MAGI in 2026 — sitting exactly at the phaseout starting line, still holding the full $12,000. They convert $100,000 to Roth. New MAGI: $250,000.

The phaseout runs its full course. Excess MAGI is $100,000, so each spouse’s $6,000 is reduced by 6% of that excess — $6,000 each, to zero. The couple’s taxable income therefore rises by $112,000 on a $100,000 conversion: the conversion itself plus the erased $12,000.

Here is the federal math on their return, using the 2026 brackets and standard deduction from IRS Rev. Proc. 2025-32 ($32,200 joint, plus $1,650 per spouse 65+, for $35,500 total):

| Return | Taxable income | Federal taxes |

|---|---|---|

| Before the conversion | $102,500 | $11,974 |

| After the conversion | $214,500 | $36,676 |

| Extra federal taxes | +$112,000 | $24,702 (24.7%) |

The decomposition matters more than the total. Had the tax break survived, the conversion alone would have cost $22,000 — exactly 22% of $100,000, exactly what a bracket-only analysis predicts, because the entire conversion sits inside the 22% band. The remaining $2,702 is the price of the erased amount: $12,000 of income that was sheltered before the conversion and taxed at 22–24% after it.

Stated as a marginal rate: inside the $150,000–$250,000 phaseout band, each dollar of MAGI adds $1.12 of taxable income. In the 22% bracket that is an effective 24.64%; in the 24% bracket, 26.88%. The bracket table shows neither number.

Assumptions behind the worked example

All baseline income is ordinary (IRA withdrawals, pension, interest) for simplicity — no Social Security benefits or capital gains in the stack. MAGI equals AGI (no tax-exempt interest or foreign exclusions), so tax MAGI and IRMAA MAGI are the same number. The couple takes the standard deduction; both spouses are 65+ by year-end 2026 with valid Social Security numbers, and both are enrolled in Parts B and D in 2028, so the IRMAA surcharge applies twice. No state taxes included. 2028 IRMAA is illustrated at 2026 thresholds and surcharge amounts held constant — a conservative simplification, since both will be inflation-adjusted upward; the surcharge conclusion holds but the 2028 dollar amounts will differ.

Part B and Part D premiums are priced off MAGI from two years earlier, so 2026 income sets 2028 premiums. Per the CMS-derived 2026 IRMAA brackets, the first surcharge tier for joint filers begins at $218,000 of MAGI. At $150,000, this couple was comfortably clear. At $250,000, they are $32,000 over the line.

The 2026 tier-1 surcharge is $81.20 per month for Part B plus $14.50 for Part D — $95.70 per person, on top of the $202.90 standard Part B premium. Because IRMAA applies per enrollee, both spouses pay it: $95.70 × 2 × 12 = $2,296.80 for the year. (Illustrated at 2026 rates held constant for 2028 — conservative, since 2028 thresholds and surcharges will both be higher; at roughly 3% annual threshold inflation the 2028 tier-1 line would sit near $231,000, still well below this couple’s $250,000.)

Treat that $2,296.80 as the floor, not the forecast. Part B premiums are among the fastest-inflating costs seniors face in retirement: they have compounded at 7.3% per year since the program began in 1966 (from $3 per month then to $202.90 now), with Part D at about 4.1% since 2006. Grow the 2026 tier-1 surcharges at those historical rates for two years and the couple’s 2028 bill comes to roughly $2,621 — with the standard Part B premium itself near $233 per month. IRMAA surcharges scale with premiums, so every year of premium inflation quietly raises the price of crossing a threshold.

Note what the senior deduction does not do here: nothing. Below-the-line amounts never touch MAGI, so even the couple’s remaining tax break — if any had survived — would offer no IRMAA protection. The only defenses are managing MAGI before year-end or, after a qualifying life event, appealing with Form SSA-44.

Add it up: $24,702 of federal taxes plus $2,296.80 of surcharges is $26,998.80 — a 27.0% all-in rate on a conversion the client believed was a 22% decision. The $4,998.80 difference is invisible to bracket math, and it arrives in two installments: one on the 2026 return, one in a 2028 premium notice.

None of this argues against Roth conversions. It argues for sizing them against all three systems at once. Two alternatives from the same starting point show the shape of the trade:

Convert $50,000 instead. MAGI lands at $200,000: the couple keeps $6,000 of the senior deduction, stays under the $218,000 IRMAA threshold, and pays $12,320 of extra federal taxes — the same 24.64% effective rate inside the phaseout band, but with zero IRMAA surcharge and half the tax break preserved.

Or convert up to $68,000. That is the most this couple can convert in 2026 without crossing the first IRMAA tier ($218,000 − $150,000). The phaseout still runs partially — at $218,000 MAGI they keep $3,840 of the original $12,000 — but the 2028 surcharge never happens.

And because IRMAA is recalculated annually from the two-year lookback, a single conversion year creates a single surcharge year. Spreading conversions across years, or capping them at thresholds, changes the outcome materially — which is exactly the kind of multi-year optimization that cannot be done on a bracket card.

Whether you evaluate RetirementAdvisorPro or build the analysis by hand, hold the process to the same standard for tax years 2025–2028. A conversion recommendation is incomplete unless it models:

RetirementAdvisorPro runs a proposed conversion through the federal brackets and the IRMAA thresholds in one pass, so the conversion-year tax and the premium consequence two years out appear in the same plan. The worked example above — taxable income rising $112,000, the $24,702 tax bill, the $2,296.80 surcharge landing in 2028 — is exactly the analysis that belongs in front of the client before anything is recommended.

Advisors use it to test conversion sizes against each IRMAA tier and bracket top, and to compare a one-year conversion against a multi-year schedule. The client sees the trade-offs as one picture instead of discovering the hidden half from a premium notice. That conversation, run before the conversion instead of after it, is what separates the advisor who modeled the whole decision from the one who modeled a bracket.

The fastest way to pressure-test this on a real household is to run one through the software. Watch the Roth conversion demo, or book a live session below and we’ll model one of your clients — conversion size and the 2028 IRMAA consequence — on the call, and walk through the deduction-phaseout math alongside it.

Then keep exploring the rules behind every conversion recommendation — the brackets, thresholds, Medicare costs, and MAGI mechanics that decide what a client actually keeps.

IRMAA & MAGI

Brackets & Premiums

Appeals & Timing

Common questions about our platform and services

Join financial advisors who are providing world-class retirement planning services with our AI-powered platform.